The Charm Process: Your Second Chance at Justice

Here's something that might shock you: Workers have 20 days to submit Request for Reconsideration after negative decisions, yet the majority of workers don't also understand this option exists. The insurer are relying on your lack of knowledge.

The WCAB procedure really prefers prepared employees. The Workers' Payment Appeals Board (WCAB) works as the judicial arm of the system, making up seven members appointed by the Guv. These courts see the exact same insurance provider strategies each day, and they're not quickly deceived.

Method that works: I lately represented a mechanic whose insurance claim was initially rejected for "pre-existing problems." We collected 10 years of clinical records showing no prior back issues, obtained witness statements from colleagues, and provided biomechanical proof clarifying exactly how the particular training occurrence triggered his injury. The Employees' Compensation Court not only approved his claim however granted maximum irreversible disability benefits amounting to $67,000.

The obligatory negotiation seminar is your negotiation advantage. Before any kind of trial, both sides must participate in a negotiation conference where a judge promotes arrangements. Insurance policy firms recognize that if they do not resolve reasonably, they risk a test where a hurt worker with strong proof commonly wins huge.

Why Insurer Auto-Deny 33% of Valid Cases (And Just How to combat Back)

Allow me share something insurance business don't want you to recognize: First case rejections affect roughly 33% of employees' compensation claims, and several of these are automatic rejections created to dissuade workers from seeking genuine advantages. suing a teen driver after accident.

The strategy is easy: reject first, examine later. Insurer know that many employees won't appeal appropriately or will certainly approve lowball settlements instead of fight. What they're not depending on is workers who comprehend the system and have correct representation.

Insurance provider have 90 days to accept or refute insurance claims, but should offer standing letters within 2 week. Throughout this period, they have to accredit approximately $10,000 in medical therapy. I have actually seen companies attempt to avoid this by slow-walking the procedure-- do not allow them.

Real case example: A vehicle motorist in Fresno harmed his back training cargo. The insurance coverage business refuted his case, specifying "insufficient clinical evidence of work-relatedness." We got the monitoring video from his company revealing the exact minute of injury, the emergency situation room documents revealing instant reporting of work injury, and statements from colleagues that observed the incident. The denial was reversed, and he got $52,000 in overall advantages.

The vital insight: The majority of rejections are based on technicalities or inadequate preliminary documentation, not the actual advantages of your instance. With appropriate lawful depiction, success prices leap from 30% for unrepresented workers to 70-90% with lawyer assistance.

What the 2025 Modifications Mean for Your Instance Right Now

The landscape has moved considerably in favor of hurt workers, however you need to act purposefully to profit. Setting up Bill 2337 updated the allures process by accrediting electronic trademarks on all Workers' Settlement Appeals Board documents, making it less complicated to submit appeals and maintain momentum in your case.

The useful advantages:

- Faster paper handling indicates quicker resolutions

- Digital filing minimizes bureaucratic hold-ups that insurer made use of to exploit

- Video hearings (starting March 2025) remove traveling obstacles for workers statewide

- Enhanced oversight implies insurer deal with higher analysis for case hold-ups

Current chance home window: Insurance provider are still adjusting to the new demands. This transitional period creates possibilities for workers who understand the modifications and have supporters that can utilize them efficiently.

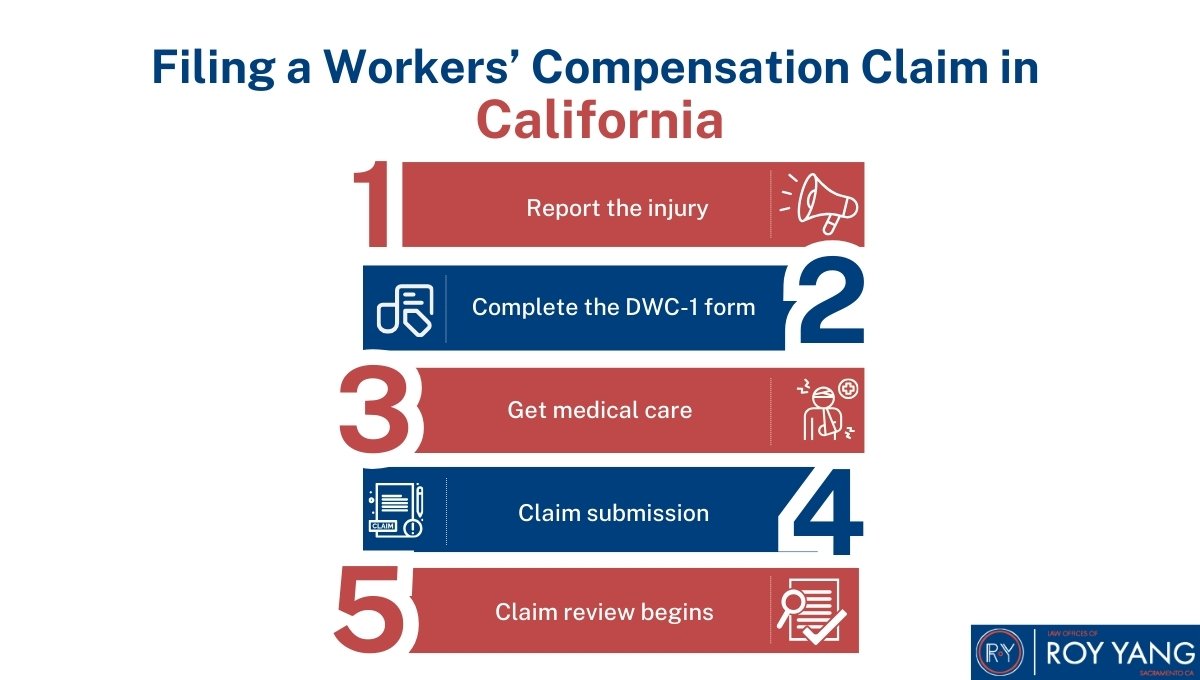

The 30-Day Guideline That Destroys More Claims Than Any Type Of Other Factor

Here's the harsh truth: Miss the 30-day injury reporting target date, and your insurance claim is dead. Duration. No exceptions, no charms, no second chances. The 30-day injury reporting deadline is absolute and can not be waived.

I've seen building and construction workers shed $150,000+ in advantages since they assumed their manager reporting the injury sufficed. It's not. You should personally inform your company in creating within 30 days. For repetitive tension injuries or job-related diseases, the clock begins when you knew or ought to have recognized the condition was occupational.

Pro suggestion from the trenches: Email your supervisor and human resources division immediately, using language like "I am officially informing you of an occupational injury that took place on [date]." Keep the read invoice. This easy e-mail has saved clients 10s of thousands when companies later asserted they were never alerted.

One client, a nurse in San Diego, created carpal passage syndrome over months of repeated charting. She discussed wrist pain to her supervisor however really did not formally report it as occupational up until 3 months later. The insurer tried to deny her insurance claim based on late reporting, but we confirmed the supervisor's understanding made up constructive notification, safeguarding a $28,000 settlement.

When You Definitely Required a Lawyer (Based Upon Actual Instance Results)

The data is clear: Success rates boost significantly with appropriate legal depiction, climbing from approximately 30% for unrepresented employees to 70-90% with lawyer support.

You need instant lawful appointment if:

- Your insurance claim is refuted (even partly)

- Your employer strikes back versus you

- You're pressured to return to work before clinical clearance

- The insurance provider stops paying advantages without description

- You're provided a settlement (never ever approve without testimonial)

- You establish issues or brand-new symptoms

- Your injury affects your ability to do your normal job

The cost framework protects you: The golden state's backup cost system needs attorney costs in between 9-15% of advantages awarded, with all fees subject to Workers' Compensation Court approval. You pay nothing ahead of time, and fees just come from what we recover for you.

Real impact of representation: A medical facility employee in Bakersfield wounded her shoulder in an individual training event. She initially attempted to handle the case herself and was used $4,000. After employing our company, we found added injuries through proper medical assessment, documented recurring work restrictions, and discussed a $38,000 settlement. Our fee was $5,700-- she netted $32,300 versus the $4,000 she would have obtained alone.

Why Is the Strategic Selection for The Golden State Employees

After 15 years in this field, I have actually seen just how the ideal lawful group changes results. The employees who accomplish the most effective results do not simply need any lawyer-- they need supporters that comprehend The golden state's complicated employees' compensation system inside and out, that remain present with legislative modifications, and that have the sources to combat major insurer.

combines deep legal expertise with real advocacy for hurt employees. We comprehend that your workers' settlement insurance claim isn't nearly cash-- it has to do with your capacity to support your family members, keep your self-respect, and protected correct treatment for injuries that might influence you for life.

Our method is various: We don't simply process paperwork. We explore every angle, create detailed clinical proof, determine all potential sources of healing, and fight strongly for maximum settlement. When insurer see standing for a claim, they recognize they're facing experienced advocates that won't approve unfair settlements.

The assessment is totally free, and you pay absolutely nothing unless we win. Offered the intricacy of California's workers' settlement system and the substantial cash at stake, getting professional guidance isn't simply clever-- it's important for shielding your legal rights and maximizing your recovery.

Your next step: Don't let insurance policy companies capitalize on your unfamiliarity with the system. Contact today for a cost-free consultation. We'll review your situation, discuss your rights under the brand-new 2025 regulations, and describe an approach to achieve the very best feasible end result for your situation.

Remember: The same injury can lead to a $5,000 negotiation or a $50,000 settlement depending on exactly how it's taken care of. Make certain you're on the best side of that formula.

The Medical Supplier Network Trap (And Just How to Retreat It)

Below's where most employees get entraped: Your employer likely has a Medical Provider Network (MPN) of medical professionals who are essentially paid to reduce your insurance claim. Workers have substantial rights in doctor choice through predesignation and Clinical Carrier Network options, however many do not recognize how to exercise these civil liberties.

The predesignation strategy: Predesignation permits workers to pick their personal doctor for work injuries if they complete DWC Type 9783 before injury takes place. I advise all my clients finish this kind immediately upon starting brand-new work. It's like insurance coverage for your workers' payment case.

Current victory: A storehouse employee in Oakland had predesignated her family members physician that had actually treated her for years. When she harmed her shoulder, the employer attempted to force her right into their MPN. We implemented her predesignation rights, and her trusted physician correctly documented the degree of her injuries, causing a $43,000 settlement versus the $5,000 the MPN medical professional suggested.

Even without predesignation, you have civil liberties. You can request a consultation within the MPN if you're unsatisfied with treatment, and you have the right to an Independent Medical Review (IMR) if therapies are rejected. Independent Medical Evaluation (IMR) gives final allure civil liberties for denied clinical therapy, and it's completely complimentary to workers.

Common Blunders That Price Workers Thousands

After seeing thousands of instances, particular errors show up over and over once more:

Blunder # 1: Accepting the very first settlement deal. Insurance coverage business generally use 30-50% of an insurance claim's real worth. I've never ever seen an initial offer that was reasonable. A painter in San Jose was offered $8,000 for a shoulder injury. After correct instance advancement, we settled for $41,000.

Mistake # 2: Not reporting all signs quickly. Your first clinical report ends up being the structure of your entire claim. If you point out only back discomfort however later on create leg pins and needles, the insurer will certainly declare it's unconnected. Always give your doctor a total image of how you feel, even if signs and symptoms seem minor.

Mistake # 3: Returning to work prematurely. I recognize the monetary stress, but returning before you're clinically gotten rid of can permanently harm your case. As soon as you return, insurance companies argue you're not impaired. A building worker in Riverside returned after two weeks with a back injury, after that re-injured himself. The insurance policy firm denied benefits for the 2nd injury, costing him $35,000.

Blunder # 4: Not understanding long-term special needs rankings. California's intricate disability score system thinks about medical impairment, line of work, and age factors. A 10% impairment rating might seem low, however, for a 50-year-old construction worker, it could indicate $25,000+ in advantages. Numerous workers accept negotiations without recognizing what their special needs score should be.

The Bottom Line: Knowledge + Depiction= Optimum Healing

The golden state's employees' payment system offers thorough benefits, yet only for employees who understand how to navigate it successfully. The 2025-2026 legislative modifications create extraordinary opportunities for hurt employees, however these benefits just profit those that know how to utilize them. The data do not exist: Represented employees constantly achieve better results, faster resolutions, and higher negotiations. A lot more notably, they prevent the disastrous blunders that can completely damage their cases and their futures. Don't become one more fact of employees that went for much less than they was worthy of. The insurer have groups of legal representatives and insurers working to minimize your insurance claim. Should not you have a knowledgeable advocate defending your maximum recovery? Call today. Your future-- and your household's financial safety-- may depend on the decisions you square away currently.

Why 2025 Is the most effective Year Yet for The Golden State Employees' Settlement Claims

The game altered totally on January 1, 2025, and the majority of employees don't even recognize it. Setting up Expense 1870 currently needs all California employers to alert staff members of their right to lawyer examination-- something insurance provider fought tooth and nail to avoid.

Below's what this indicates for you: Every work environment needs to now show updated DWC Type 7 posters explicitly specifying that you deserve to talk to a licensed lawyer which lawyer costs are typically paid from your healing, not out of your pocket. This isn't simply paperwork-- it's a fundamental shift that levels the having fun area.

I lately had a client in Los Angeles who was informed by her employer that working with a lawyer would "complicate things" and delay her benefits. Under the brand-new legislation, that employer was legitimately called for to notify her of her attorney rights. When we used this offense as utilize, her case went for $34,000 rather than the preliminary $8,000 deal.

The numbers promote themselves: Temporary disability advantages enhanced 3.8% for 2025, with maximum weekly settlements climbing from $1,619.15 to $1,680.29. For an employee gaining $80,000 yearly that's off benefit six months, this boost alone adds over $900 to their overall recovery.

The The Golden State Employees' Payment Guide Every Injured Employee Demands (2025-2026)

California's employees' compensation system refined 363,900 office injuries in 2023 with $16. [:kw7].7 billion in failures, making it among the nation's most extensive worker defense systems. The 2025-2026 legislative modifications have fundamentally moved the playing area for injured employees-- yet just if you recognize how to use them to your benefit

What I'm sharing right here isn't academic recommendations from a textbook. These are battle-tested approaches from actual cases, including the usual errors that cost employees thousands and the insider knowledge that divides effective claims from rejected ones.

The Negotiation Figures They Do Not Want You to See

Let's chat cash-- since that's what this is truly about. Typical settlement amounts in The golden state variety from $2,000 to $40,000, with many employees receiving in between $2,000 and $20,000. Here's what those statistics do not inform you: the distinction in between the reduced end and high end frequently comes down to representation and technique.

**

Actual settlements from my method:

- Head injury situations: Ordinary $93,942

- Numerous body part injuries: Average $62,859

- Amputations: Average $126,000

- Back injuries with appropriate documents: $25,000-$ 75,000

- Repetitive stress injuries: $15,000-$ 45,000

The surprise multiplier result: Many employees do not understand that their workers' compensation insurance claim might likewise set off third-party liability claims. A roofing professional who fell due to a malfunctioning safety belt received $35,000 in employees' compensation benefits however an extra $280,000 from the tools producer. This is why very early lawful consultation is crucial-- we can identify all prospective sources of recovery.

Among my clients, a distribution driver, was rear-ended while making a delivery. His employees' comp situation worked out for $28,000, however the third-party car insurance claim versus the various other driver cleared up for an additional $150,000. Without comprehending both systems, he would certainly have missed out on $150,000 in recovery.